Azimuth BTC Strategy

Azimuth Quant is a quantitative research initiative focused on systematic digital-asset allocation strategies designed for long-term investors.

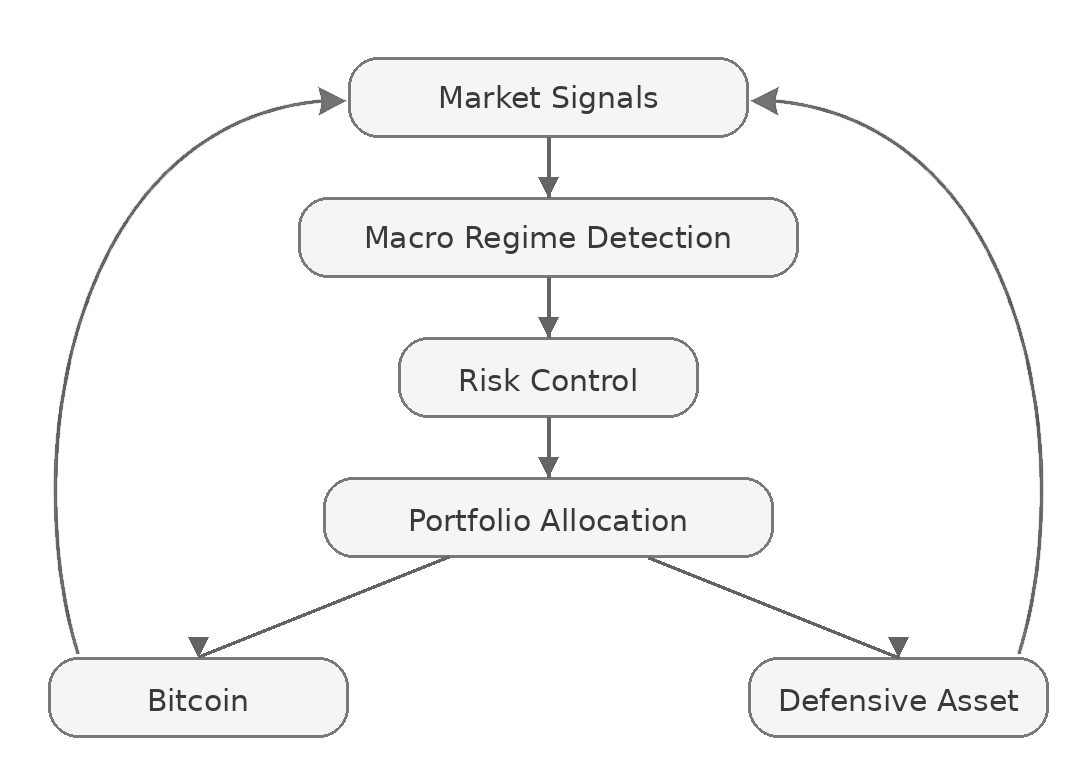

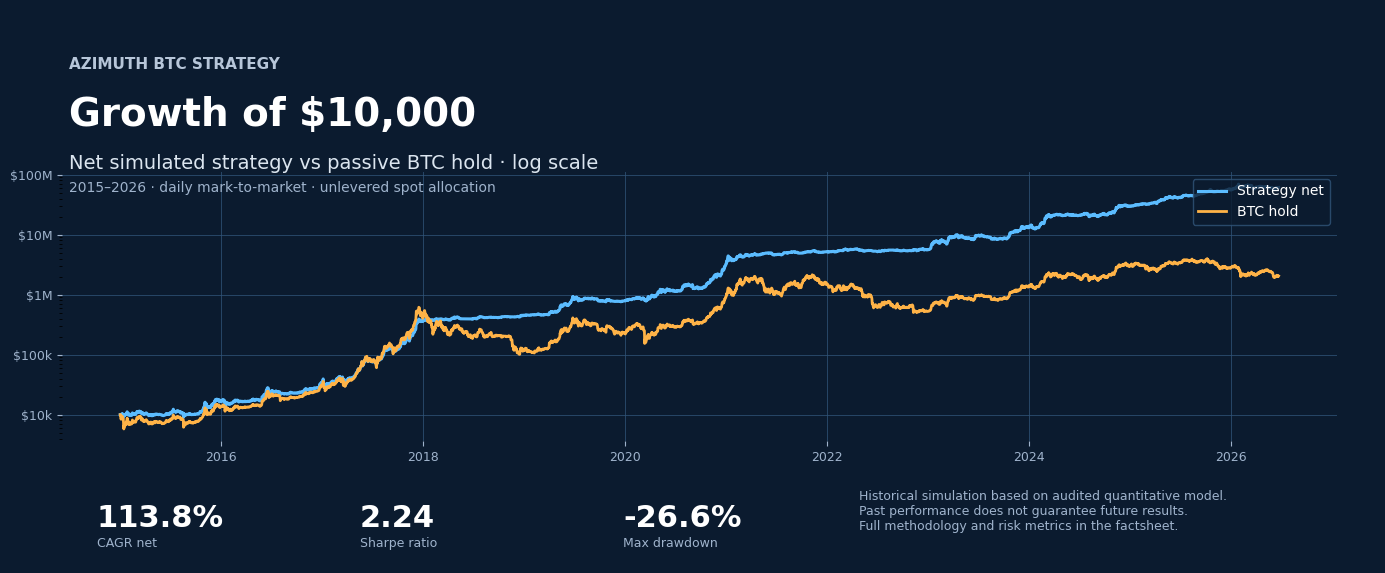

The Azimuth BTC Strategy is a systematic BTC/PAXG/USDT allocation model designed to dynamically adjust Bitcoin exposure across market regimes.

The model increases BTC exposure during favorable conditions and can shift capital toward PAXG and USDT during adverse environments, using predefined quantitative rules rather than discretionary opinions.

A systematic alternative to passive Bitcoin exposure, designed to capture long-term upside while reducing large drawdowns through disciplined allocation.