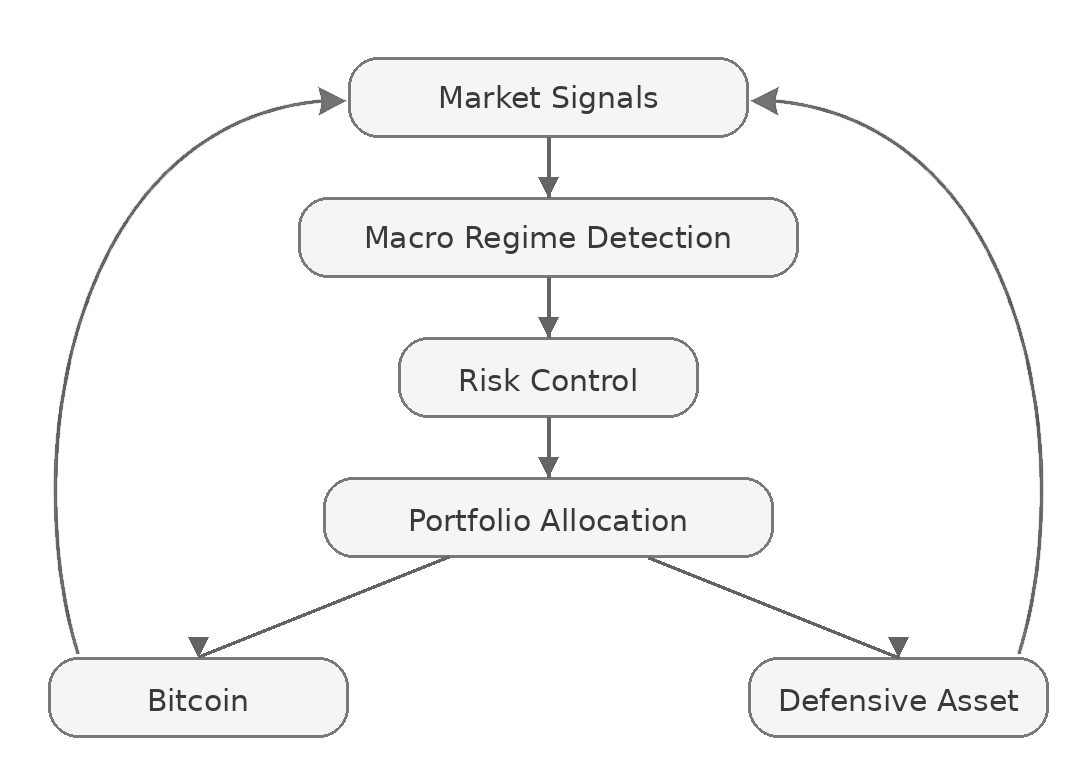

Strategy Process

Bitcoin markets exhibit large regime shifts and periods of extreme volatility. Static exposure can therefore lead to significant drawdowns during adverse market phases.

A systematic allocation framework allows exposure to adapt dynamically, increasing Bitcoin participation during favorable regimes while shifting capital toward a defensive asset during periods of elevated risk.