4. Statistical Methods for Regime Detection

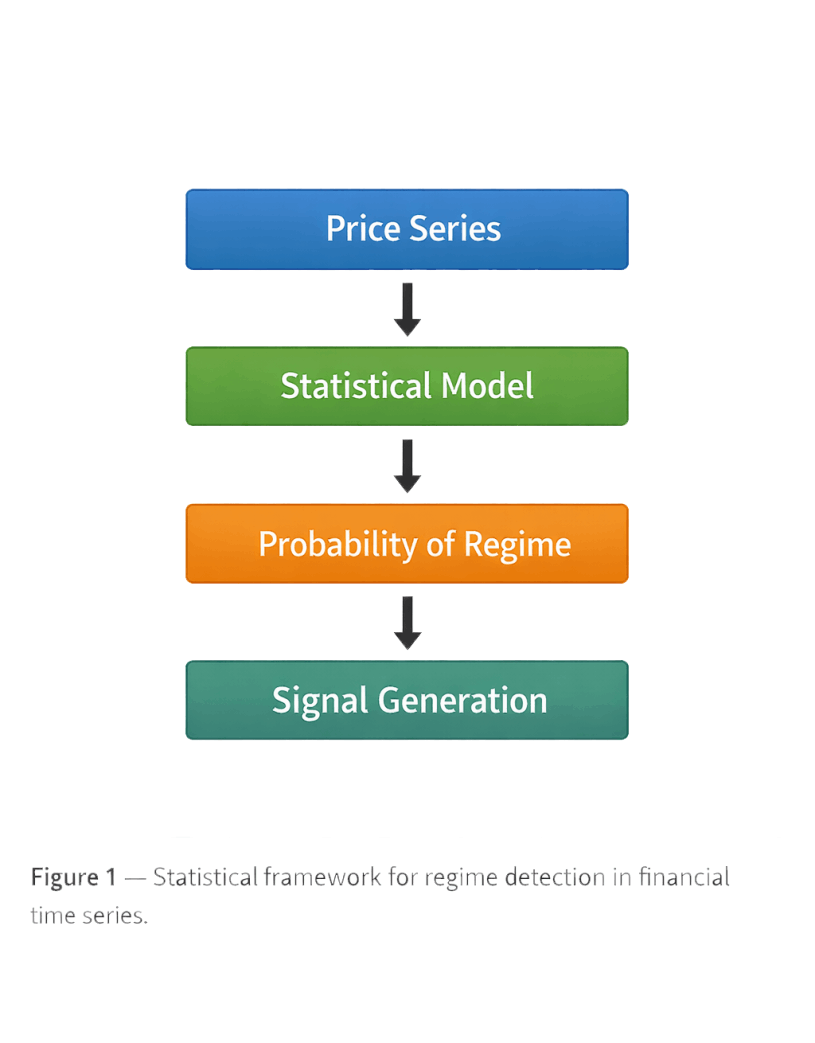

Multiple quantitative approaches facilitate the identification of these transitions. Markov regime-switching models remain prevalent due to their ability to treat regime transitions as a stochastic process governed by a transition matrix.

Alternative methodologies include Hidden Markov Models (HMM), GARCH-based volatility regime models, and structural break tests. Recent implementations in the cryptocurrency space confirm that Bitcoin’s volatility is not merely persistent but strictly regime-dependent, requiring models that can adapt to rapid changes in market variance.