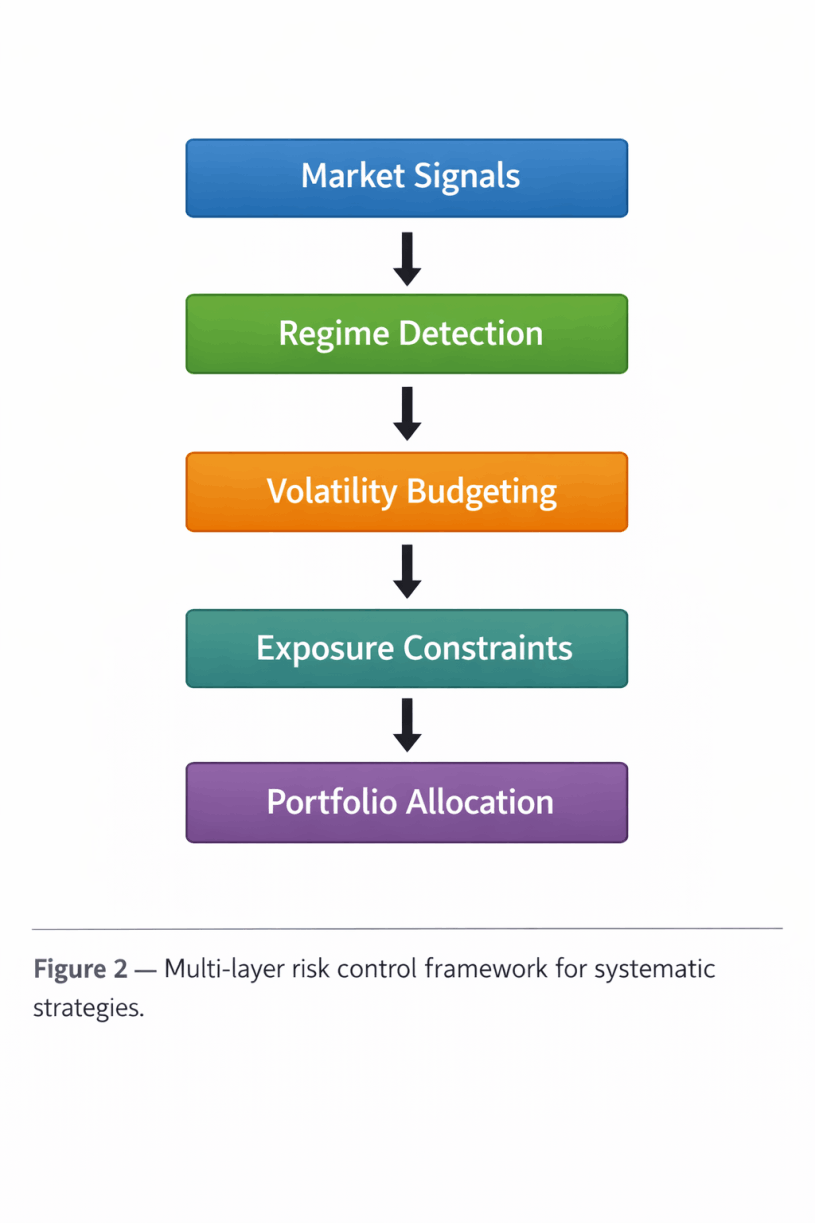

4. Volatility Targeting and Risk Budgeting

An effective methodology for managing this risk involves volatility-adjusted position sizing. Instead of maintaining a fixed allocation, the position size is scaled according to current market movement.

This approach, known as volatility targeting, helps stabilize the return profile. The logic is consistent: when volatility spikes, exposure is reduced to protect the capital base. In addition, when the market stabilizes, the position can be expanded. This ensures the total risk of the portfolio remains within a predefined budget.