Azimuth Tactical Strategy

Executive Summary (Net Base Case)

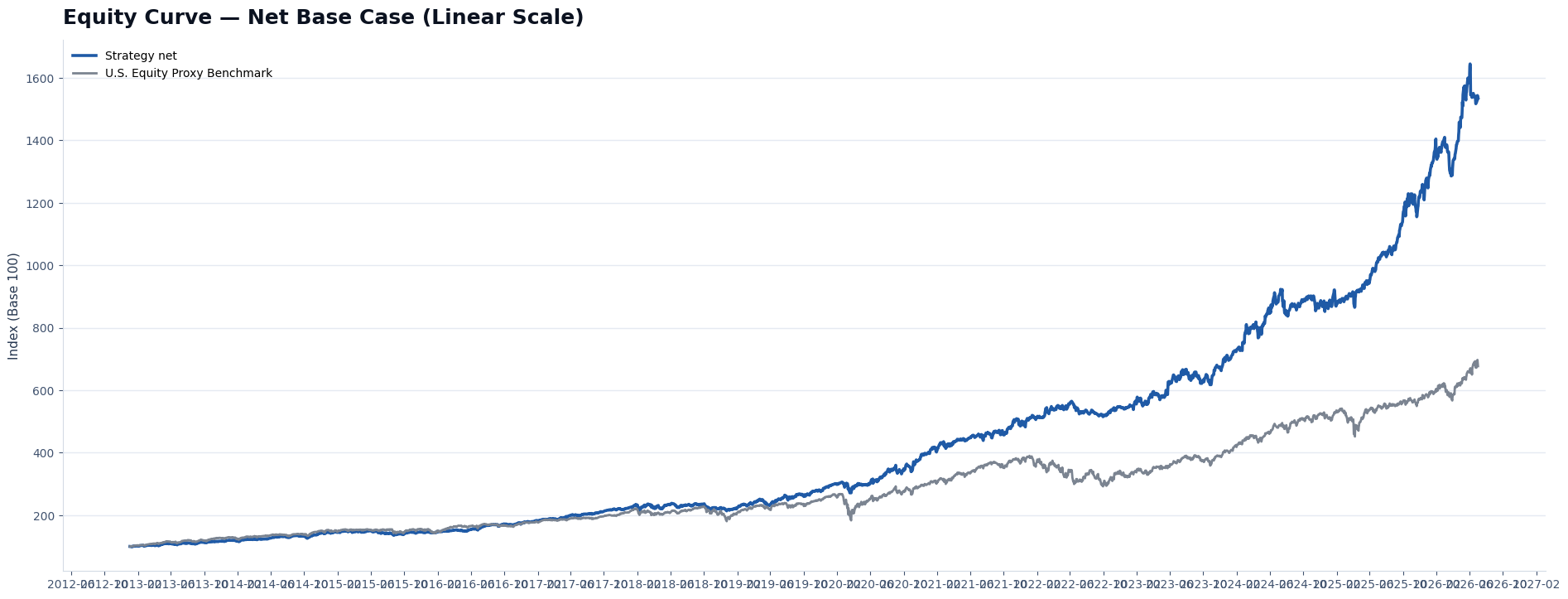

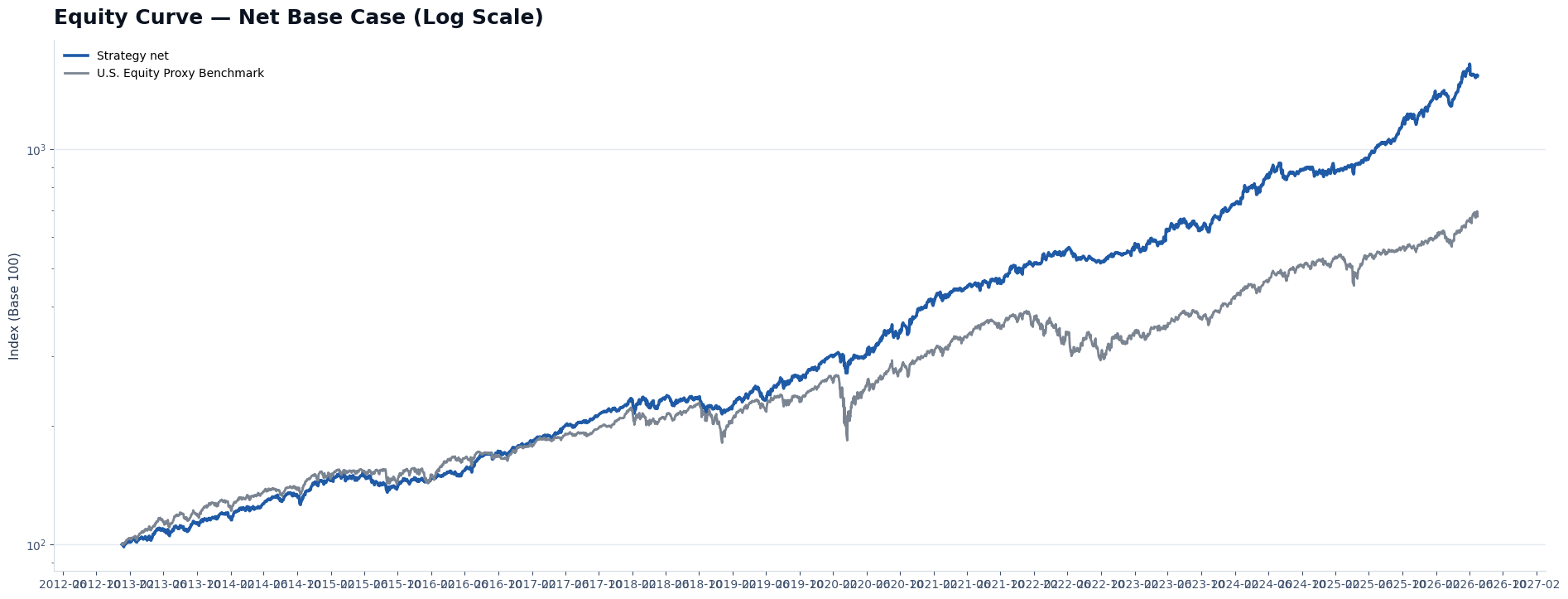

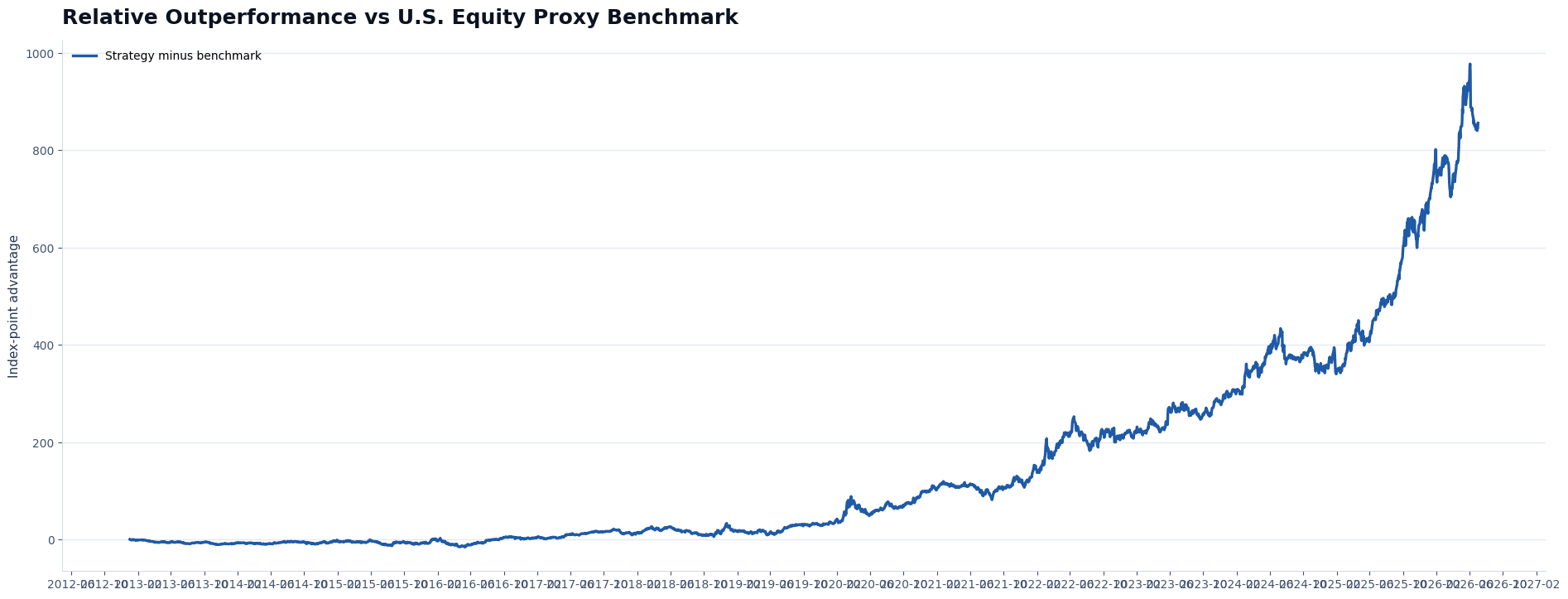

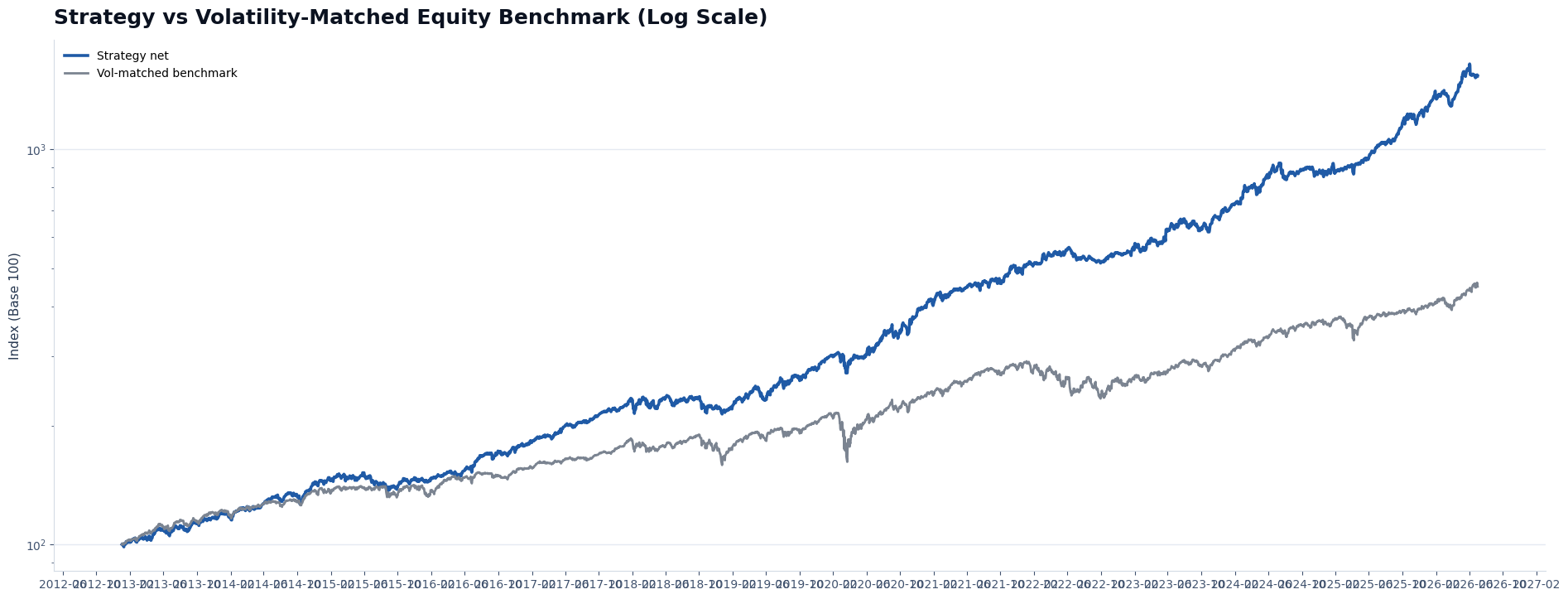

Equity Curve (Net Base Case)

Data & Methodology

Execution Model: The base model assumes a fully funded brokerage implementation using liquid, exchange-traded instruments. Operational timing is D+1: signal at close D, target/order for the next session open, then market return after execution. No leverage, margin borrowing or derivative funding is required in the base NAV.

Public Benchmarking: The public benchmark is a U.S. Equity Proxy Benchmark: an unmanaged public equity reference used as a familiar market comparison. The benchmark uses dividend-adjusted historical data, with distributions assumed reinvested. Strategy components are described by portfolio role in the public material, with implementation instructions provided to approved clients.

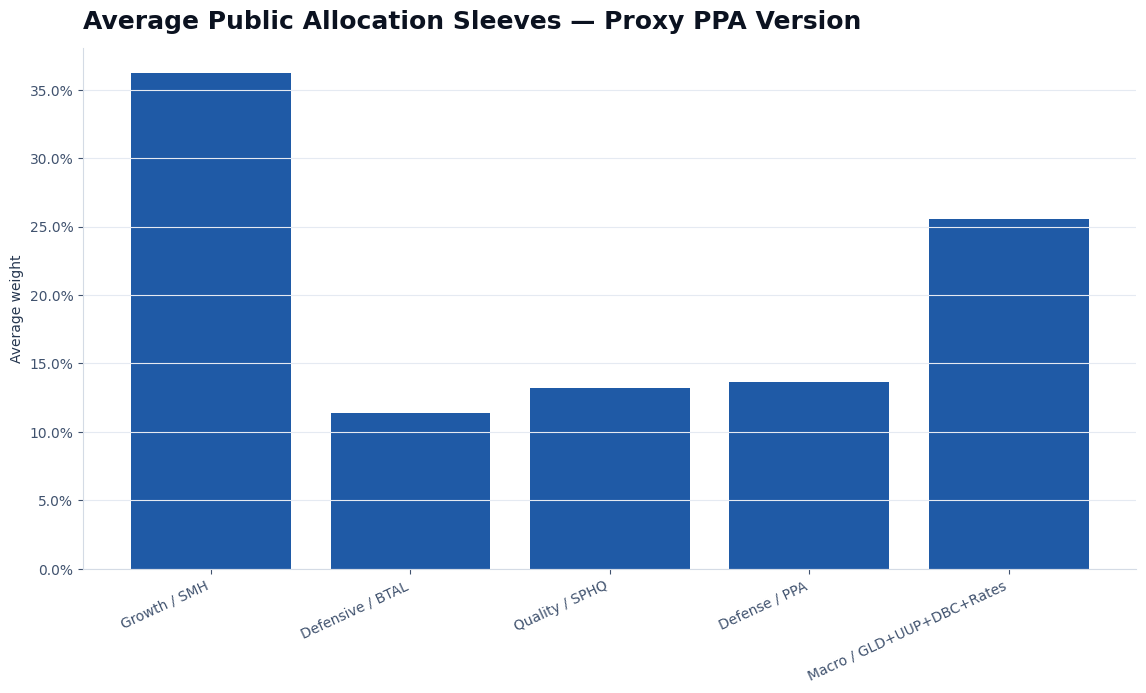

Proxy Disclosure: This version uses a PPA-only proxy structure. The portion that would otherwise be assigned to the additional defense sleeve is incorporated into PPA, allowing a longer public historical evidence window while keeping the same tactical and macro allocation architecture.

Turnover / Costs: Cost tests use consolidated executed allocation events and an additional round-trip spread/slippage stress model. The base engine already includes a brokerage-style commission estimate.

Backtest Window: September 2023 – July 2026. Performance is calculated from daily historical closes, net of modeled execution costs, with decisions applied by the engine rather than manually selected after the fact.

Dividend Treatment: Strategy components and public benchmarks are calculated from dividend-adjusted historical price series where applicable, with distributions assumed reinvested. Results should be interpreted as reinvested total-return-style simulations, net of modeled execution costs for the strategy base case.

Key Metrics (Strategy vs Public Benchmarks)

| Series | Final Multiple | CAGR | Max DD | Volatility | Sharpe-like | Calmar | Ulcer Index | VaR 95% Daily | CVaR 95% Daily | Max Recovery Days |

|---|---|---|---|---|---|---|---|---|---|---|

| Strategy Net Base Case | 15.33× | 22.47% | -11.36% | 12.72% | 1.77 | 1.98 | 0.03 | -1.18% | -1.87% | 210 days |

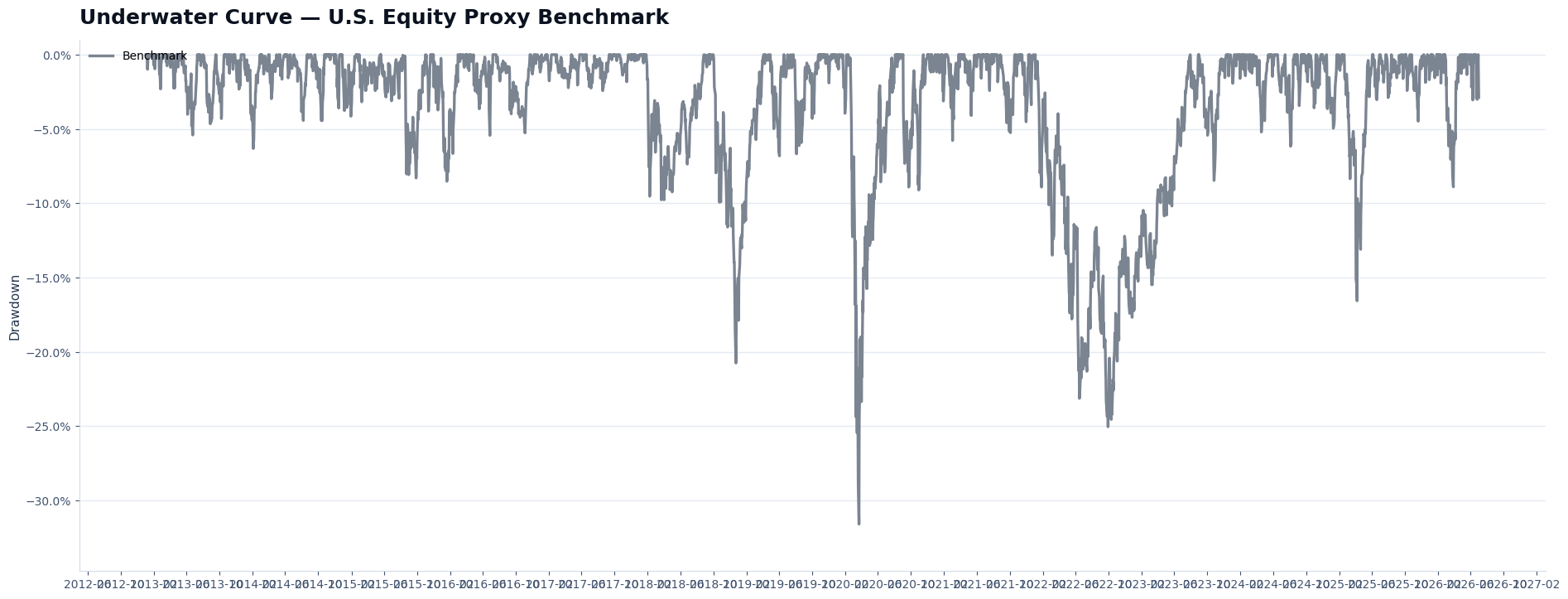

| U.S. Equity Proxy Benchmark | 6.77× | 15.26% | -31.59% | 16.55% | 0.92 | 0.48 | 0.06 | -1.52% | -2.47% | 392 days |

Daily Tail Risk: VaR & Expected Shortfall

VaR 95% Daily is the 5th percentile of historical daily net returns over the full backtest window. A value of -1.19% means that, historically, about 5% of daily observations were worse than that threshold.

CVaR / Expected Shortfall 95% Daily is the average daily loss inside that worst 5% tail. It is usually more informative than VaR because it looks beyond the threshold and measures the severity of the tail.

These are one-day tail diagnostics, not worst-case loss estimates. They do not capture all liquidity gaps, implementation constraints, tax effects, future regime changes or model risk.

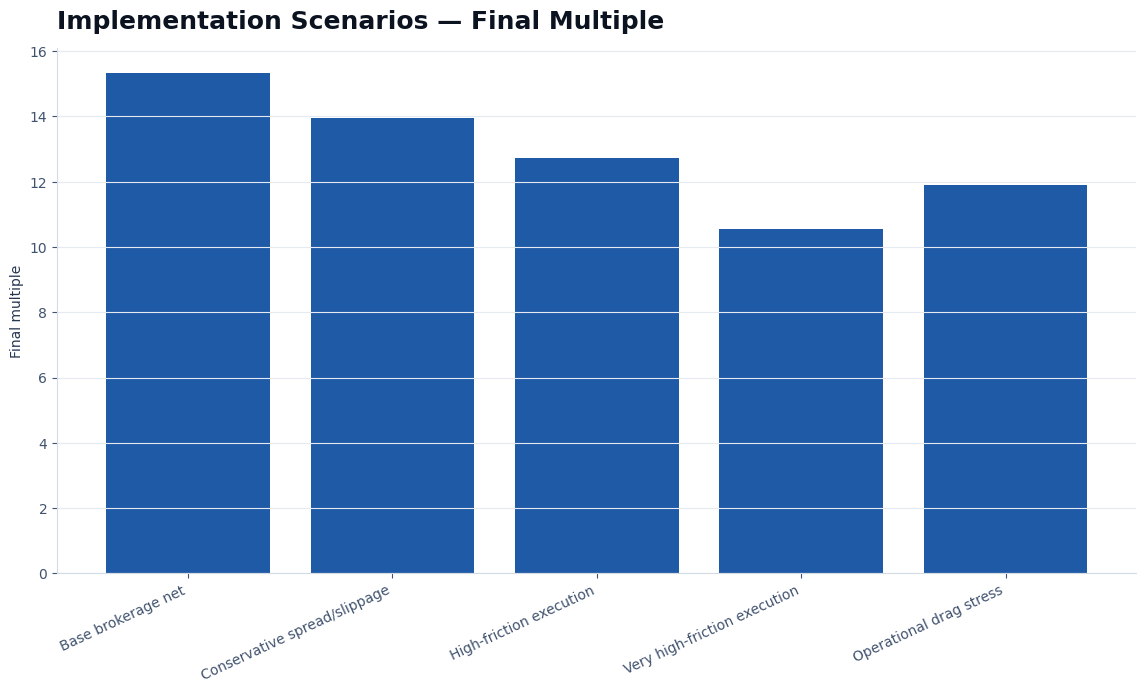

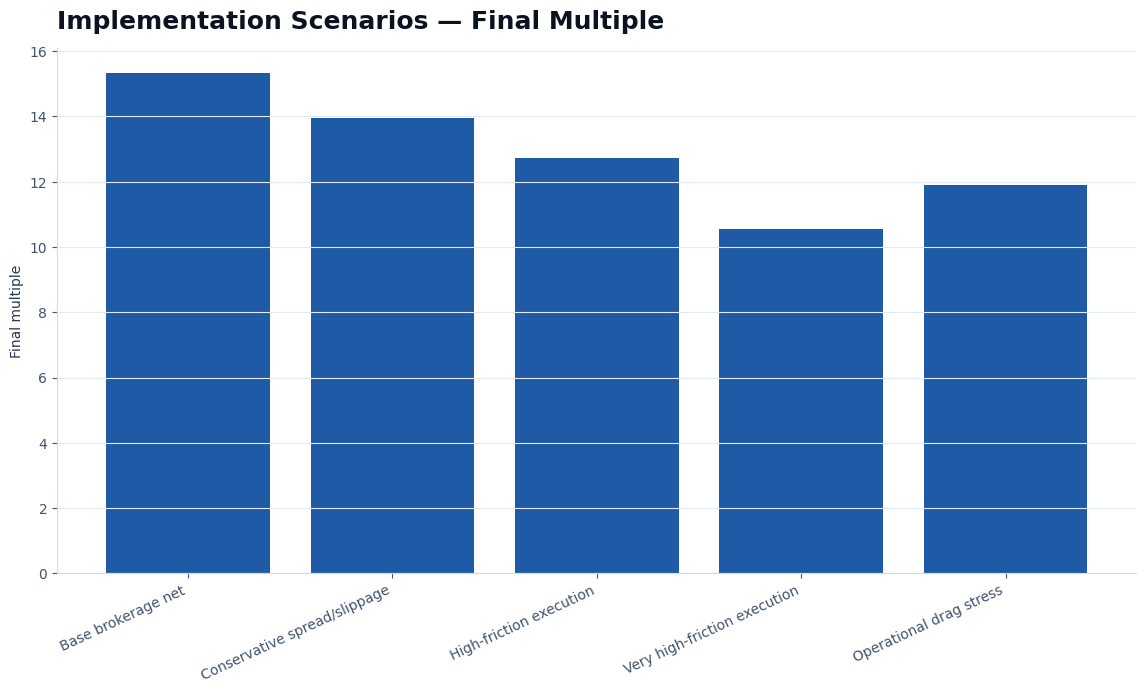

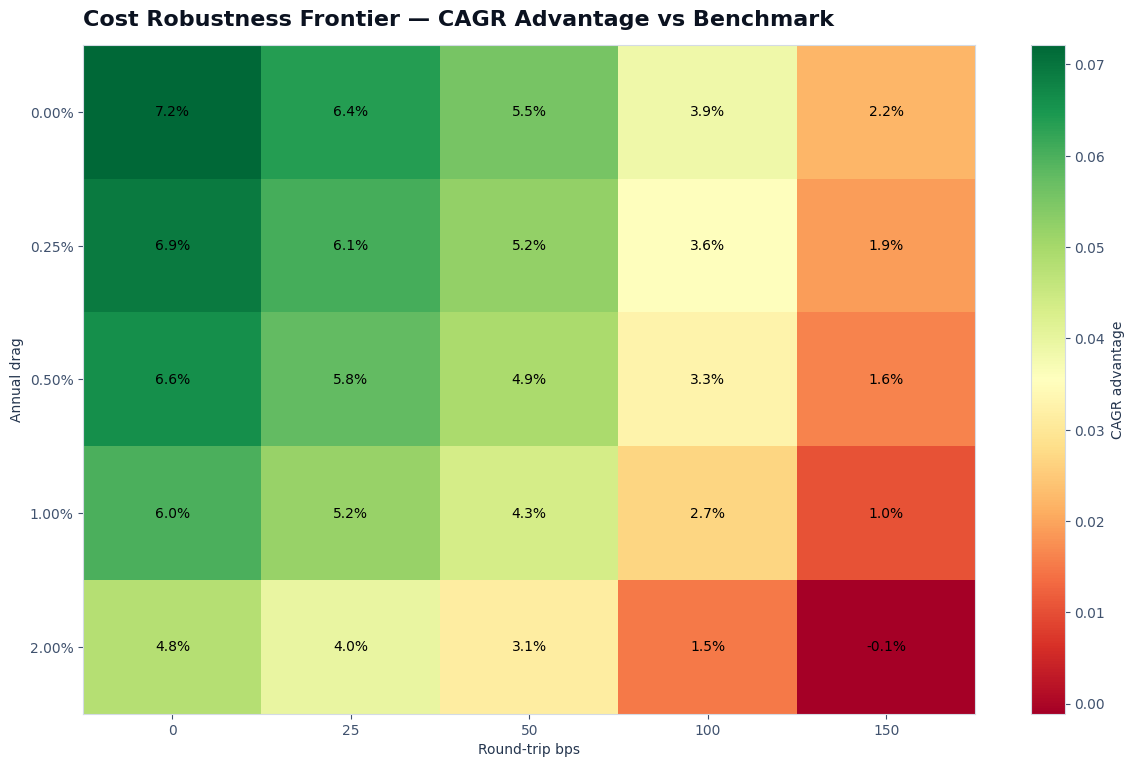

Implementation Scenarios & Execution Costs

| Scenario | Round-trip bps | Annual drag | CAGR | Max DD | Final Multiple |

|---|---|---|---|---|---|

| Base brokerage net | 0 | 0.00% | 22.47% | -11.36% | 15.33× |

| Conservative spread/slippage | 25 | 0.00% | 21.62% | -11.45% | 13.96× |

| High-friction execution | 50 | 0.00% | 20.78% | -11.53% | 12.72× |

| Very high-friction execution | 100 | 0.00% | 19.12% | -11.70% | 10.55× |

| Operational drag stress | 50 | 0.50% | 20.18% | -11.57% | 11.89× |

Out-of-Sample Validation (Time-Based Holdout)

| Period | Series | CAGR | Max DD | Volatility | Calmar | Sharpe-like | Final Multiple |

|---|---|---|---|---|---|---|---|

| Development | Strategy | 19.69% | -11.36% | 12.33% | 1.73 | 1.60 | 8.61× |

| Development | U.S. Equity Proxy Benchmark | 14.56% | -31.59% | 16.52% | 0.46 | 0.88 | 5.10× |

| Out-of-sample | Strategy | 46.80% | -8.79% | 15.51% | 5.32 | 3.02 | 1.77× |

| Out-of-sample | U.S. Equity Proxy Benchmark | 21.29% | -16.57% | 16.84% | 1.29 | 1.26 | 1.33× |

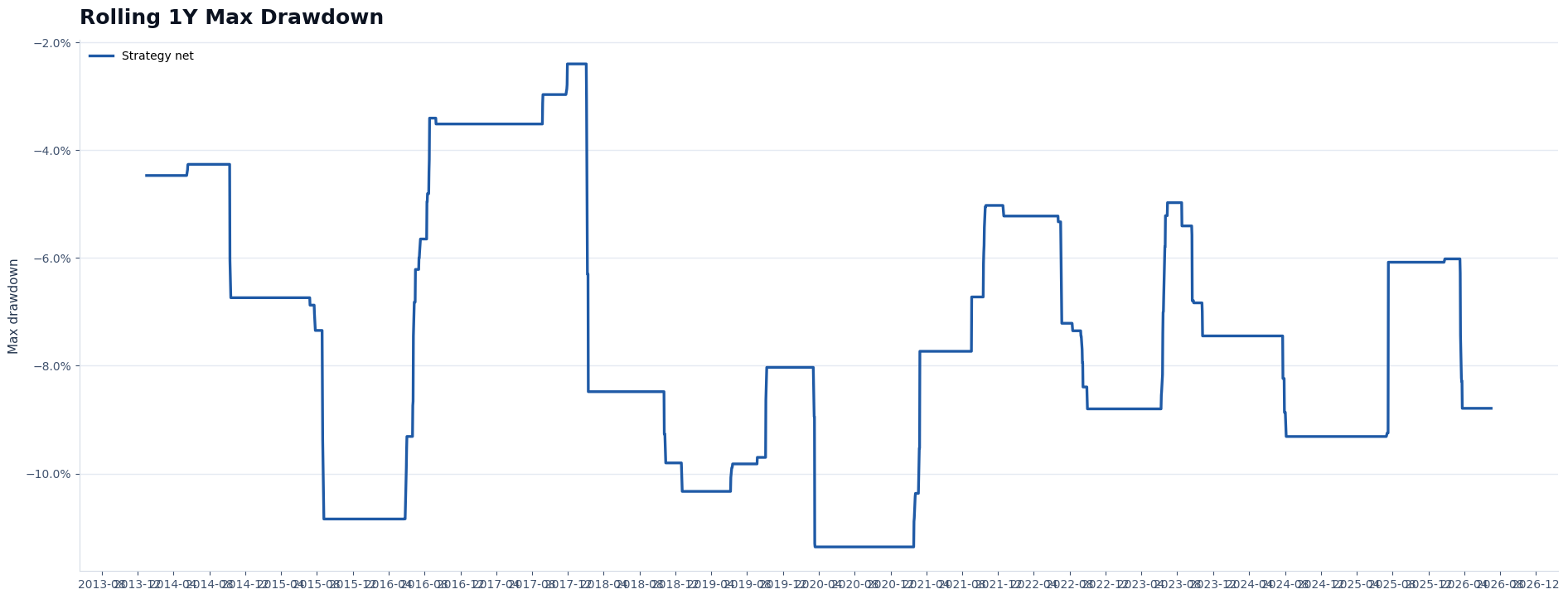

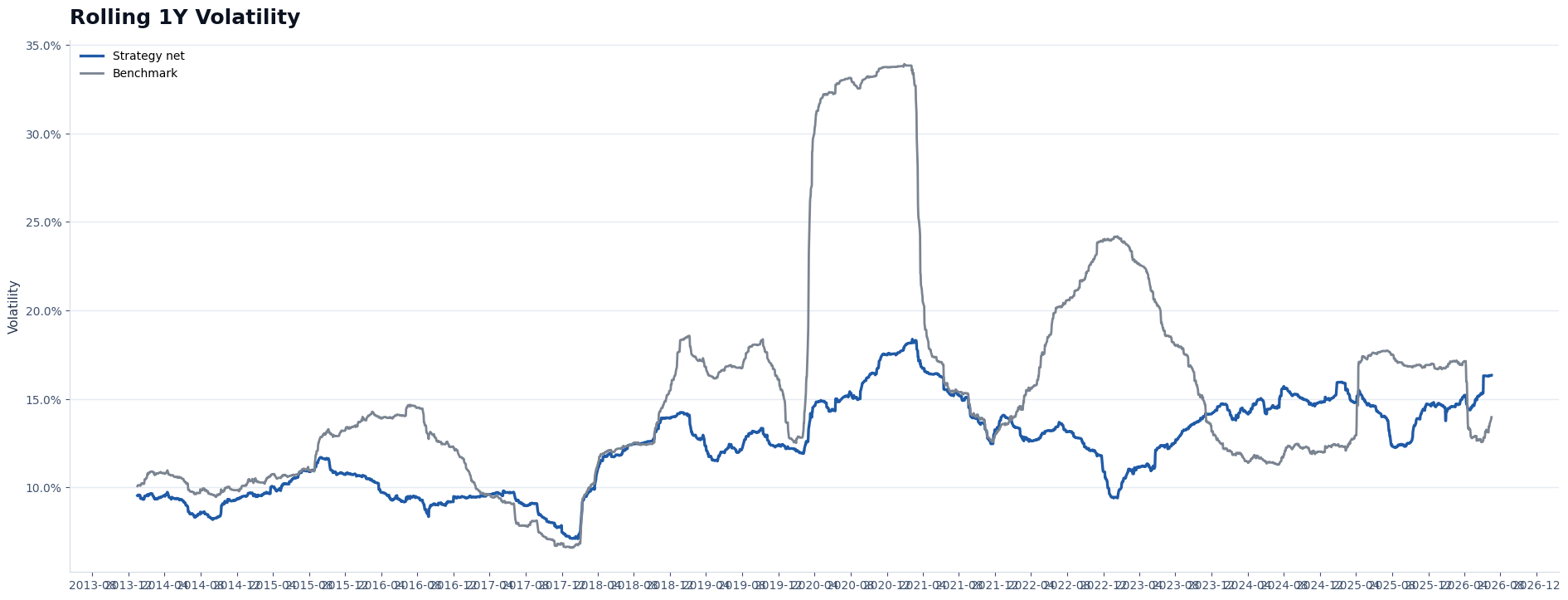

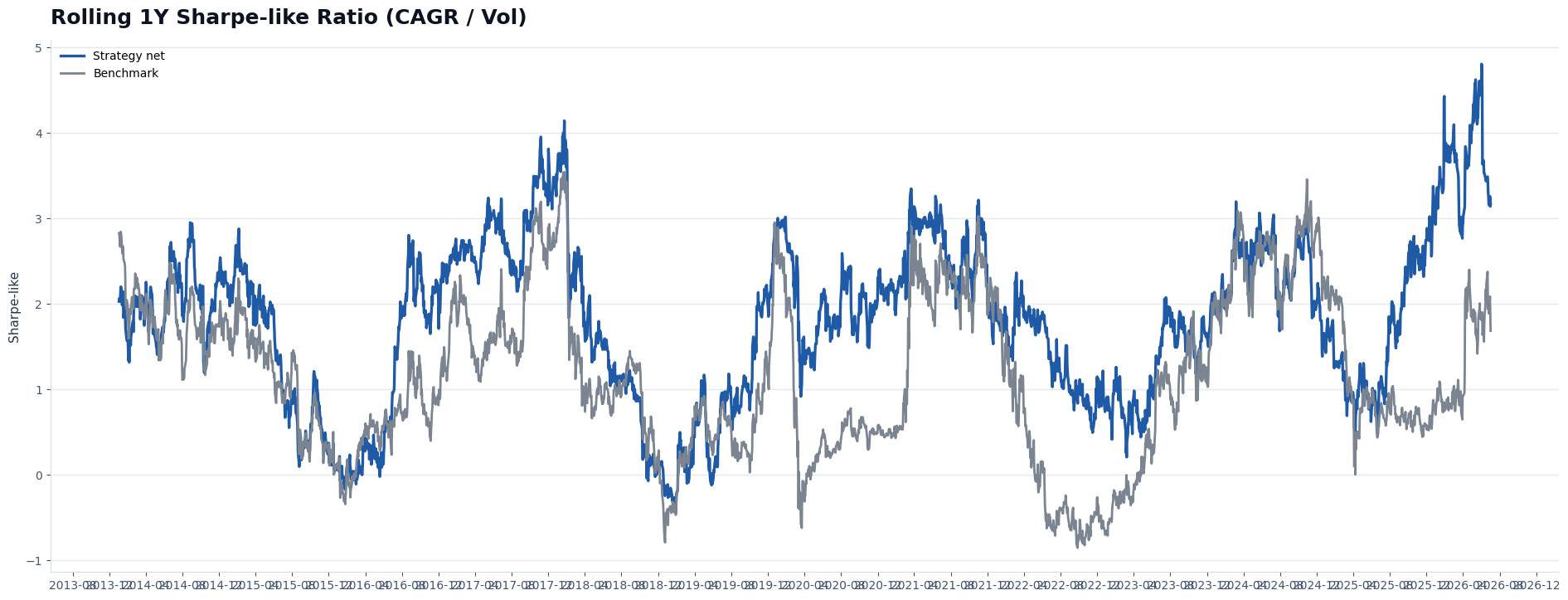

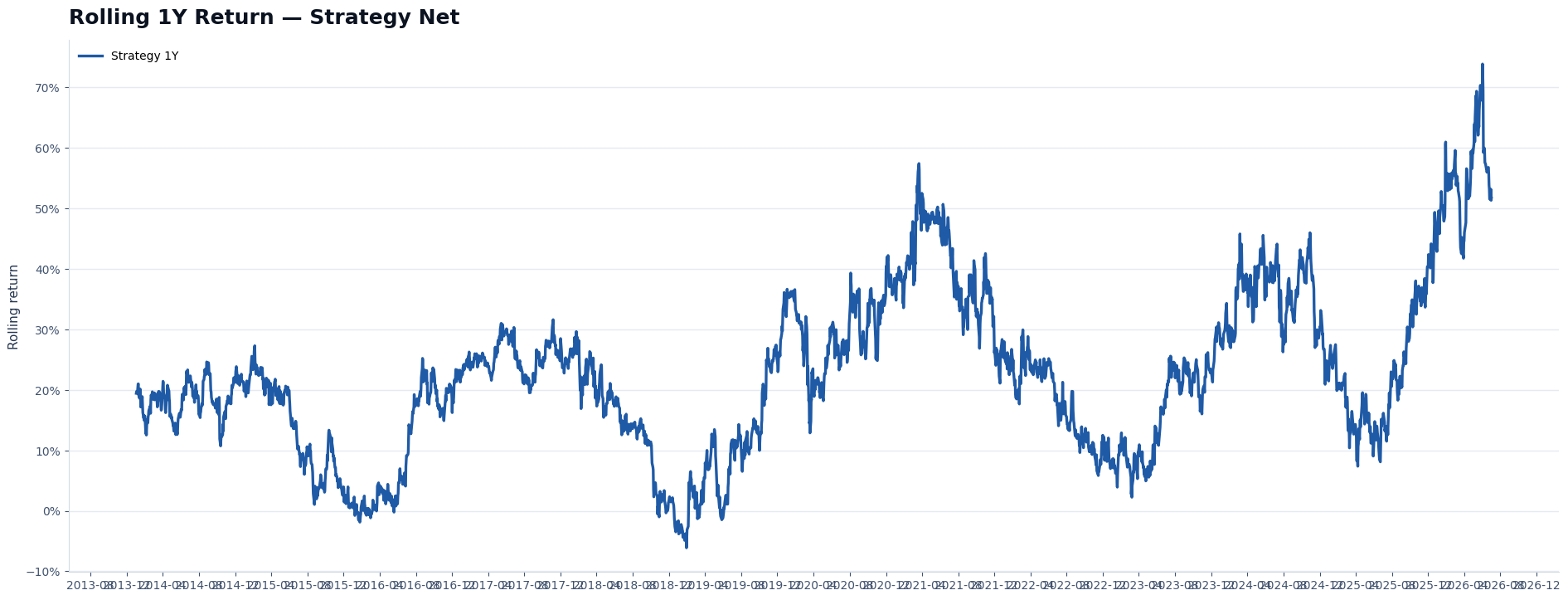

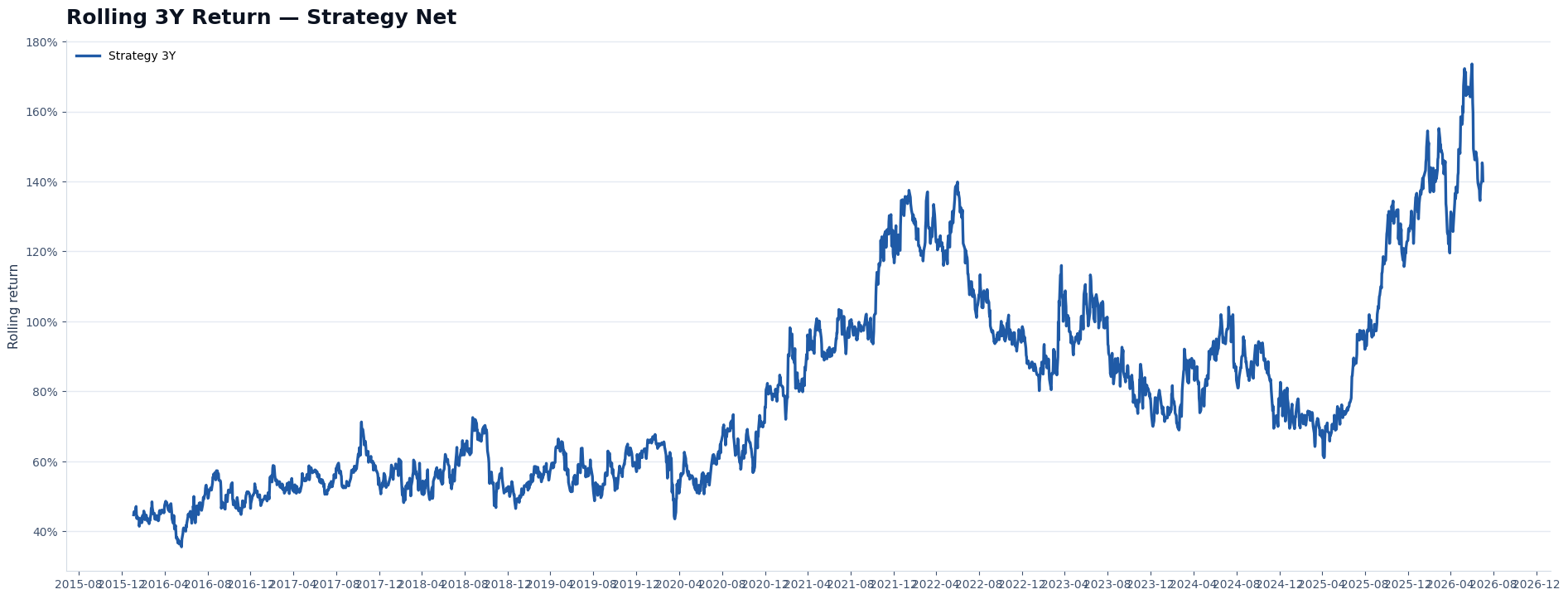

Rolling Stability (1Y)

Methodology & Investment Discipline

The model was evaluated through full-period metrics, time-based holdout, rolling windows, drawdown analysis, cost stress, synthetic stress transformations, regime analysis and block-bootstrap Monte Carlo. The public factsheet summarizes whether the behavior is robust with emphasis on robustness, discipline and investability.

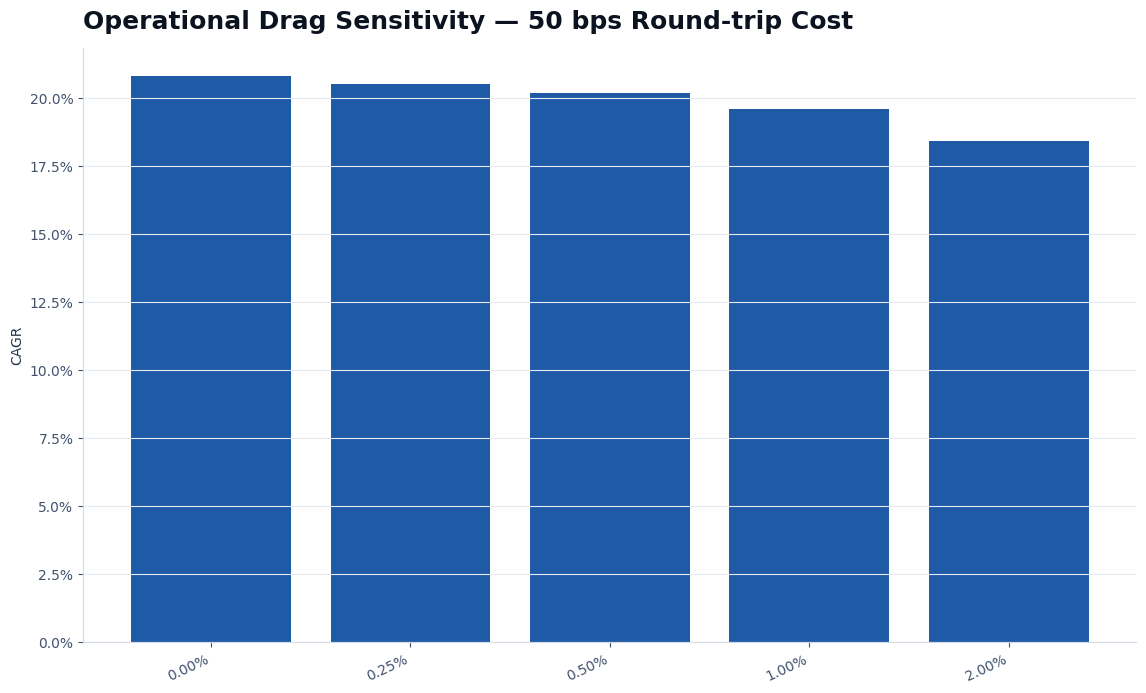

Fees & Slippage Sensitivity

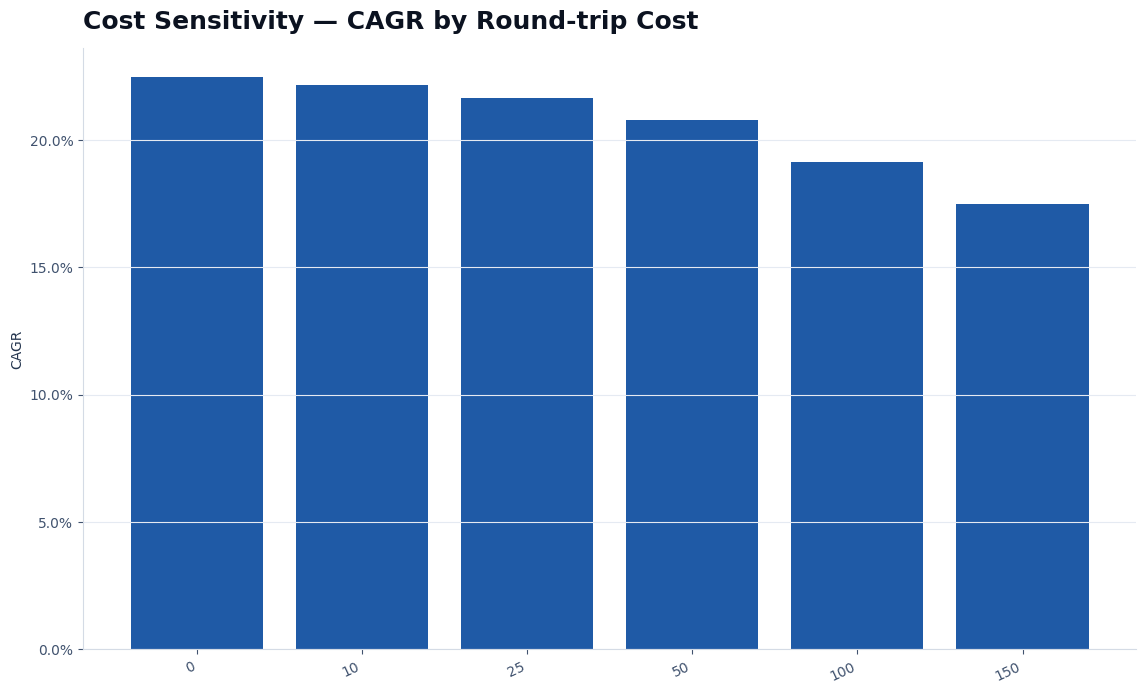

| Round-trip Cost (bps) | CAGR | Max DD | Final Multiple |

|---|---|---|---|

| 0.0 | 22.47% | -11.36% | 15.33× |

| 10.0 | 22.13% | -11.40% | 14.77× |

| 25.0 | 21.62% | -11.45% | 13.96× |

| 50.0 | 20.78% | -11.53% | 12.72× |

| 100.0 | 19.12% | -11.70% | 10.55× |

| 150.0 | 17.47% | -12.06% | 8.74× |

Implementation Scenarios

Cost Robustness Frontier

Cost Sensitivity

| Scenario | Round-trip bps | Annual drag | CAGR | Max DD | Final Multiple |

|---|---|---|---|---|---|

| Base brokerage net | 0 | 0.00% | 22.47% | -11.36% | 15.33× |

| Conservative spread/slippage | 25 | 0.00% | 21.62% | -11.45% | 13.96× |

| High-friction execution | 50 | 0.00% | 20.78% | -11.53% | 12.72× |

| Very high-friction execution | 100 | 0.00% | 19.12% | -11.70% | 10.55× |

| Operational drag stress | 50 | 0.50% | 20.18% | -11.57% | 11.89× |

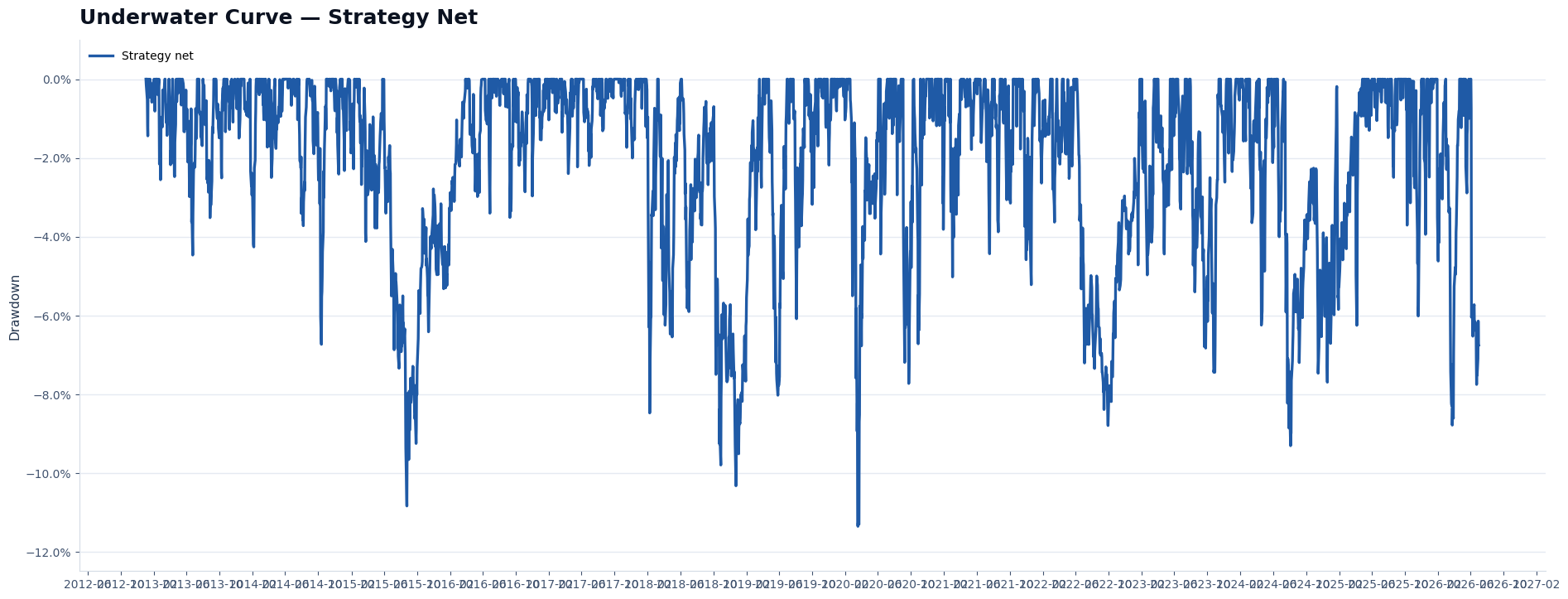

Probability of Ruin & Recovery After Shock

| Diagnostic | Result | Interpretation |

|---|---|---|

| Historical ≥80% impairment | 0.00% | No historical path fell below 20% of starting capital. |

| Monte Carlo ≥80% impairment | 0.00% | 1,000 block-bootstrap paths, 21-day blocks. |

| Negative rolling 12M windows | 2.23% | Frequency of 1-year windows with negative strategy return. |

| Negative rolling 36M windows | 0.00% | Frequency of 3-year windows with negative strategy return. |

| Worst drawdown episode | -11.36% | Peak 2020-02-19, trough 2020-03-19, recovery 2020-06-03. |

Synthetic Stress Scenarios

| Scenario | Series | CAGR | Max DD | Volatility | Calmar | Final Multiple |

|---|---|---|---|---|---|---|

| Base realized path | Strategy | 22.47% | -11.36% | 12.72% | 1.98 | 15.33× |

| Base realized path | U.S. Equity Proxy Benchmark | 15.26% | -31.59% | 16.55% | 0.48 | 6.77× |

| Volatility x1.5 | Strategy | 21.23% | -21.46% | 19.08% | 0.99 | 13.37× |

| Volatility x1.5 | U.S. Equity Proxy Benchmark | 13.29% | -45.17% | 24.82% | 0.29 | 5.37× |

| Volatility x2.0 | Strategy | 19.52% | -32.67% | 25.44% | 0.60 | 11.04× |

| Volatility x2.0 | U.S. Equity Proxy Benchmark | 10.59% | -56.87% | 33.10% | 0.19 | 3.88× |

| One-day -20% portfolio shock | Strategy | 20.95% | -22.04% | 13.77% | 0.95 | 12.96× |

| One-day -20% portfolio shock | U.S. Equity Proxy Benchmark | 14.28% | -38.99% | 17.20% | 0.37 | 6.04× |

| Sideways / zero drift | Strategy | -0.81% | -41.61% | 12.72% | -0.02 | 0.90× |

| Sideways / zero drift | U.S. Equity Proxy Benchmark | -1.36% | -46.86% | 16.55% | -0.03 | 0.83× |

Stress Comparison vs U.S. Equity Proxy Benchmark

Robustness & Risk

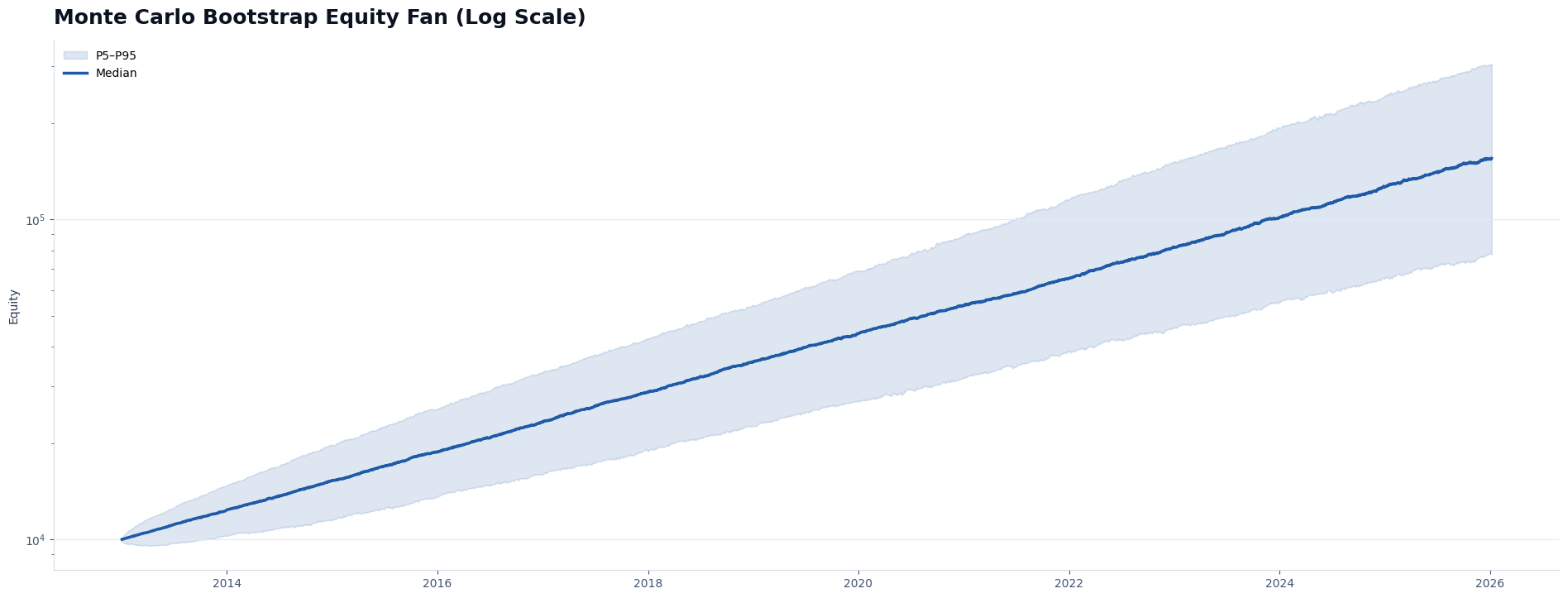

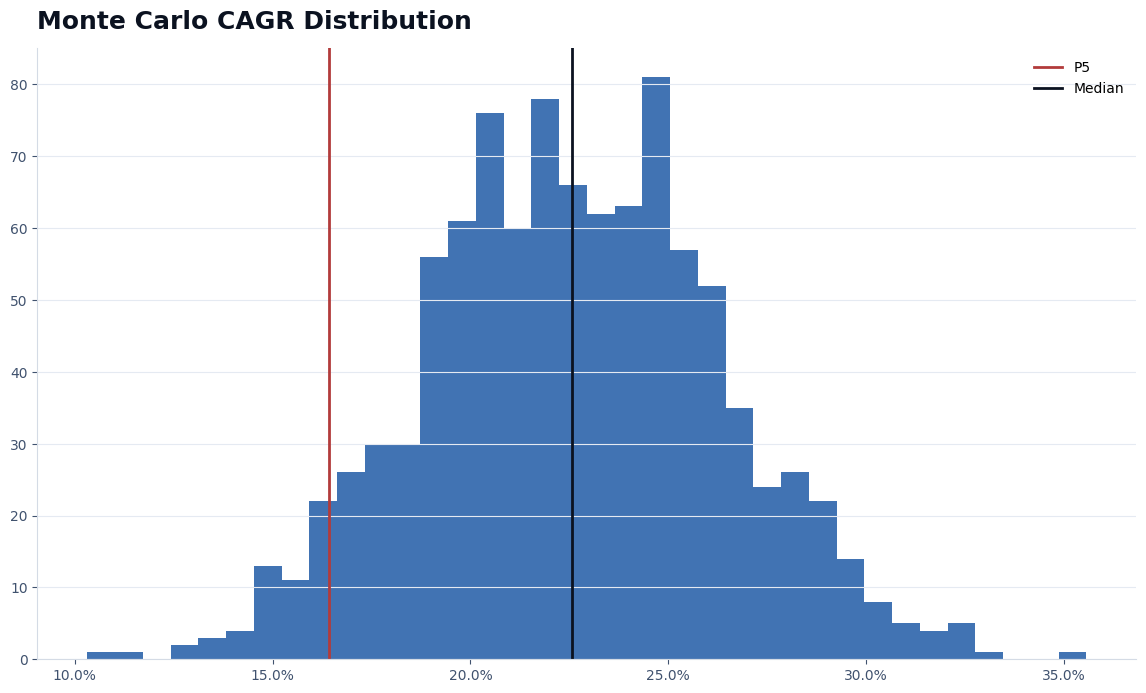

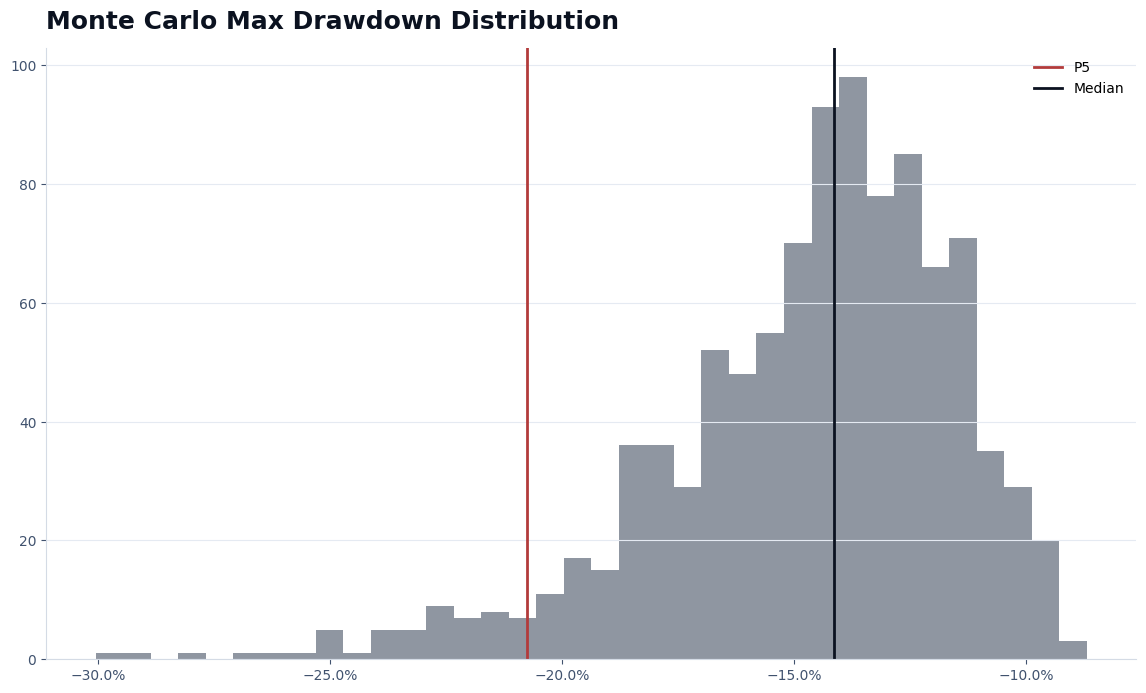

Monte Carlo (Bootstrap)

Runs: 1,000 · Block size: 21 trading days

CAGR P5 / Median / P95: 16.42% / 22.57% / 28.91%

Max DD P5 / Median / P95: -20.77% / -14.14% / -10.43%

Probability of positive CAGR: 100.00% · Probability CAGR > 10%: 100.00%

Regime Analysis (Bull / Bear / Sideways) — Strategy vs S&P 500-style Benchmark

| Regime | Series | Days | CAGR | Max DD | Volatility | Calmar |

|---|---|---|---|---|---|---|

| Bull / Risk-On | Strategy | 2529 | 34.94% | -9.31% | 12.50% | 3.75 |

| Bull / Risk-On | U.S. Equity Proxy Benchmark | 2529 | 31.19% | -8.92% | 12.07% | 3.50 |

| Bear / Risk-Off | Strategy | 507 | -11.32% | -29.99% | 14.22% | -0.38 |

| Bear / Risk-Off | U.S. Equity Proxy Benchmark | 507 | -33.82% | -60.46% | 30.51% | -0.56 |

| Sideways / Transitional | Strategy | 359 | -1.39% | -14.69% | 11.59% | -0.09 |

| Sideways / Transitional | U.S. Equity Proxy Benchmark | 359 | 3.07% | -20.12% | 15.20% | 0.15 |

Investor Fit

- Long-term systematic capital growth with explicit drawdown control.

- Participation in broad risk-on regimes without relying on permanent full equity beta.

- A rules-based allocation process with diversified defensive behavior across regimes.

- Evidence of robustness through rolling windows, stress tests, cost sensitivity, holdout analysis and Monte Carlo.

- Guaranteed capital preservation or guaranteed returns.

- Maximum public equity beta in every uninterrupted bull market.

- Short-term trading signals, market timing advice or daily discretionary calls.

- Ad-hoc rule changes outside the formal research and review protocol.

Strategy Profile

The model is designed as a systematic, rules-based and relatively low-turnover allocation framework, not as a high-frequency trading system.

Its objective is to capture persistent growth regimes while controlling downside through defensive allocation, macro rotation and exposure management when market conditions deteriorate.

The public evidence shows a materially lower historical drawdown than the U.S. Equity Proxy Benchmark, a stronger Calmar ratio than the public benchmark and positive behavior in out-of-sample years, while still acknowledging that an public equity exposure can outperform during uninterrupted equity bull markets.

The model is structurally designed for multiple regimes: risk-on participation, risk-off defense, transitional periods, volatility spikes and cost-stressed execution.

Capacity & Liquidity Considerations

The strategy is designed around liquid, exchange-traded exposures and consolidated allocation changes. It avoids excessive turnover and does not depend on microstructure edge.

- Primary implementation: liquid exchange-traded instruments through a standard brokerage account.

- Turnover: moderate, with consolidated allocation events and a minimum-order filter in the engine.

- Cost modeling: base brokerage-style commission estimate plus additional spread/slippage and drag stress.

- Capacity: expected to scale with underlying market liquidity and execution discipline; final capacity assessment should be verified under NDA with actual instruments.

Review & Optimization Protocol

Governance objective: preserve the strategy as a systematic, tested and traceable research process. The review protocol monitors degradation, execution risk, data quality and structural market changes without turning the model into discretionary optimization.

Recommendation: do not change parameters simply because time passed. The safer process is a full biennial research review plus ongoing monitoring. Logic remains frozen unless evidence shows a real structural change and a candidate passes robustness gates.

Monthly / quarterly monitoring: rolling 1Y/2Y/3Y returns, rolling drawdown, realized volatility, signal-health diagnostics, missing-data checks, cost/slippage sensitivity, average exposure drift, turnover and return concentration.

Every two years: re-run the full backtest with the same warm-up logic, refresh rolling/stress/Monte Carlo/bootstrap/delay/cost studies and only then evaluate whether adaptive adjustments are justified.

Change gates: any candidate must improve robustness without materially worsening Max DD, Ulcer, worst 1Y/2Y, average drawdown, trade concentration or execution burden.

Ongoing Review & Internal Validation

Review process: Azimuth Tactical Strategy is maintained through a systematic research and monitoring framework that evaluates performance quality, drawdown behavior, turnover, costs, rolling stability and regime sensitivity.

Validation: visible net base case reflects the current D+1 strategy evidence: Final equity $153,296, final multiple 15.33×, Net CAGR 22.47%, Max DD -11.36%, Calmar 1.98, Sharpe-like 1.77, Volatility 12.72%, Ulcer Index 0.03, and final date 2026-07-02.

Historical proxy note: this public version uses the PPA-only proxy structure: the portion that would otherwise be assigned to the additional defense sleeve is incorporated into PPA, allowing a longer historical evidence window while preserving the same allocation architecture.

Institutional statement: the strategy is presented as a systematic, rules-based and continuously reviewed allocation process. It is designed for disciplined long-term implementation, not for discretionary market timing or guaranteed future performance.

Institutional Notes (Methodology & Interpretation)

All performance figures are historical simulations and are not guarantees of future returns. Backtests are sensitive to data quality, execution assumptions, tax treatment, liquidity and future market structure.

The strategy is built around a disciplined allocation framework, recurring internal review and rules-based execution. The objective is to keep the investment process consistent across different market regimes while controlling drawdowns and avoiding ad-hoc decisions.

Approved clients receive practical execution instructions when a portfolio adjustment is required.