Azimuth Tactical Strategy

Systematic multi-asset spot strategy for serious investors: fully funded, rule-based, diversified across roles, and operated manually through private Telegram alerts with clear implementation instructions.

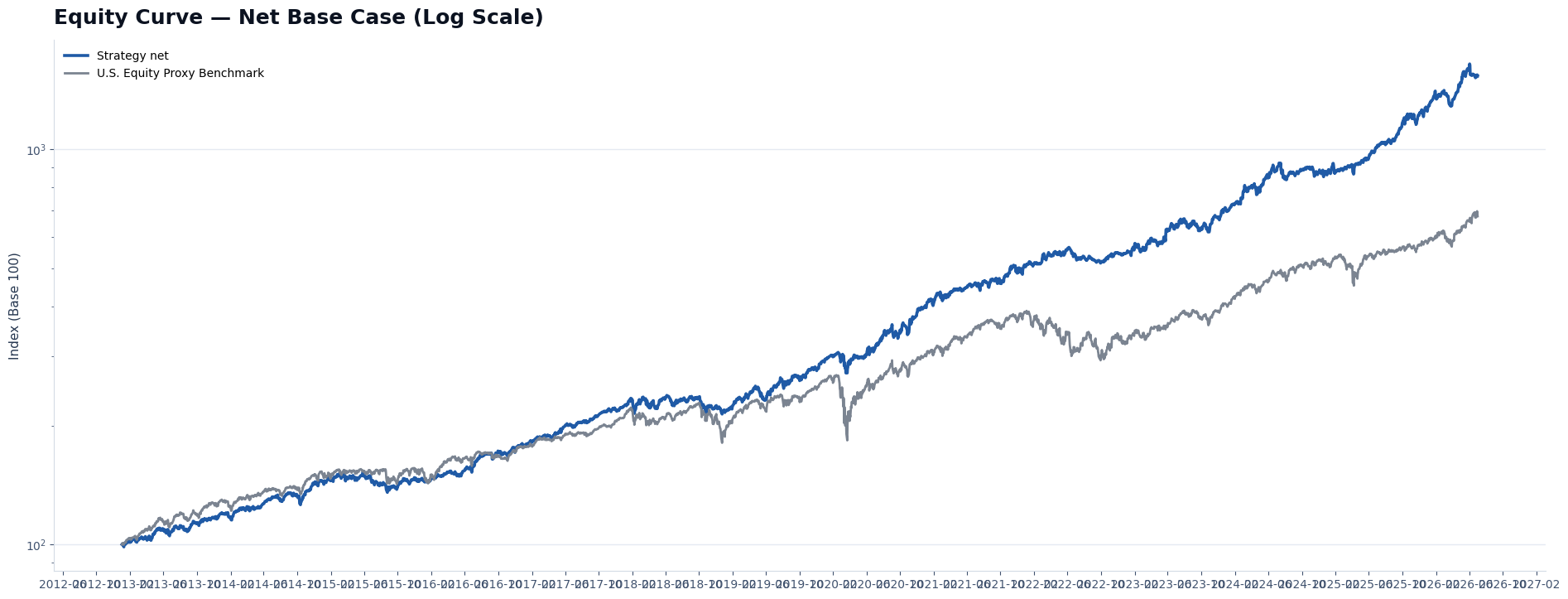

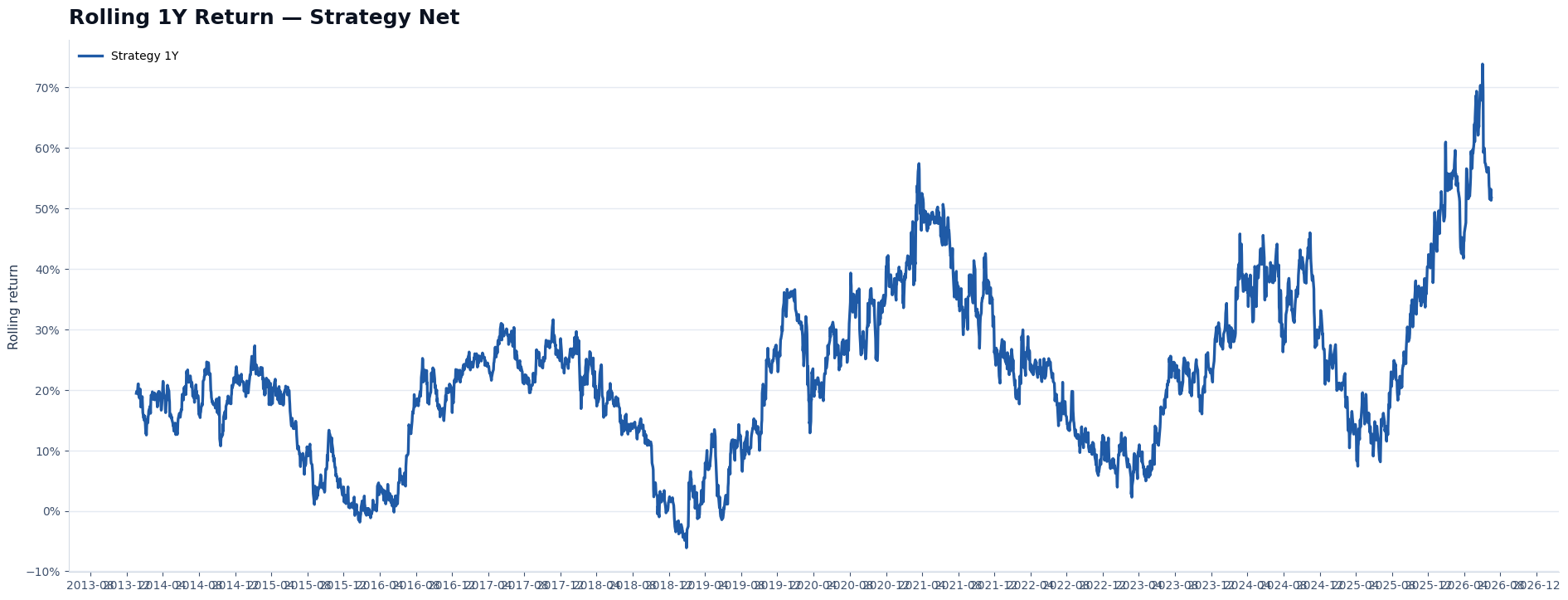

Backtest period 2013-01-02 → 2026-07-02. D+1 operational results are shown for investor evaluation and should be read together with the full risk disclosure.

A disciplined multi-asset engine built through extensive research.

Azimuth Tactical Strategy combines a core growth sleeve with defensive and macro-sensitive roles. Its rules are designed to participate when market structure is favorable, moderate aggressive exposure when risk expands, and keep the portfolio diversified across different economic environments.

The strategy was developed through extensive historical testing, practical operating checks and ongoing internal evaluation. The goal is to offer serious investors a structured allocation process instead of ad-hoc discretionary decisions.

Investors who want discipline, structure and a serious process.

The strategy is intended for investors able to follow consolidated allocation alerts, maintain broker discipline, tolerate drawdowns and evaluate the strategy over a medium-to-long-term horizon.

It is not a high-frequency trading system, not a leveraged product and not a discretionary stock-picking service.

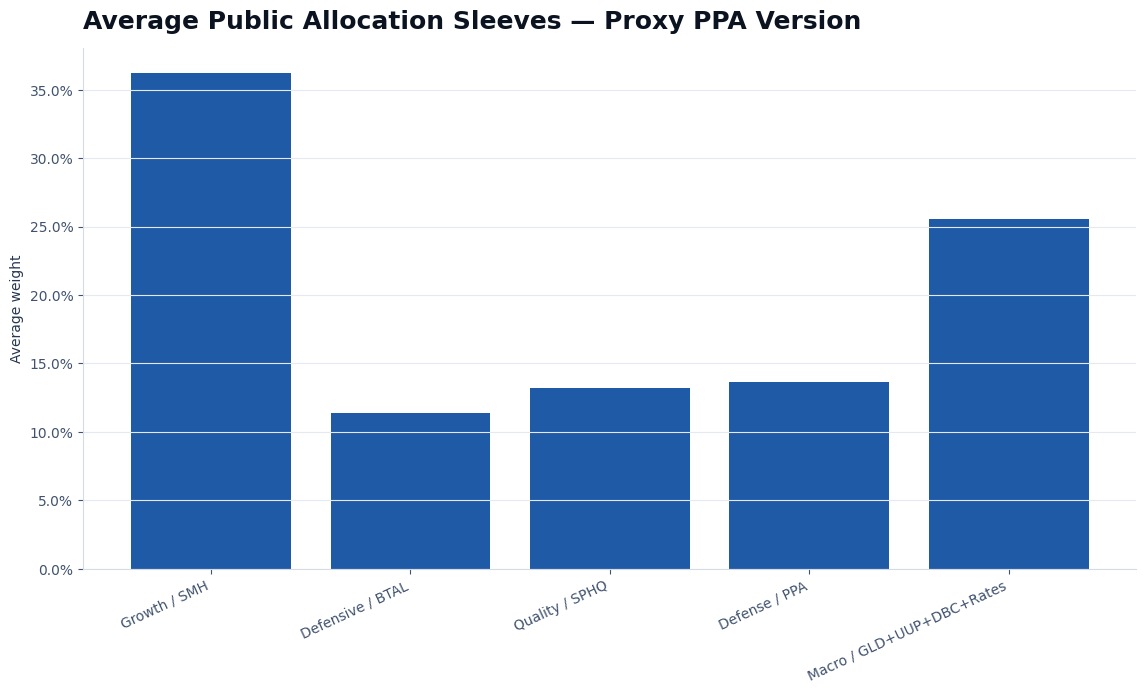

Intelligent allocation roles

Growth participation

Participates in structural growth leadership when the regime remains supportive.

Defensive buffer

Seeks to reduce portfolio fragility during equity stress and volatility expansion.

Quality/resilience

Maintains stabilizing exposure designed to avoid a purely binary risk-on/risk-off profile.

Macro rotation

Allocates among broad macro-sensitive roles as conditions evolve.

Subscribers receive target-allocation instructions in a practical format. The public page focuses on the investment process, investor suitability and risk profile.

Why not just hold a passive diversified portfolio?

Passive diversified portfolios can work well in normal environments, but they often adapt slowly when market regimes change. During periods of stress, correlations can rise and several assets may decline at the same time.

Azimuth Tactical Strategy was designed to be more adaptive. It combines growth exposure, defensive components and macro-sensitive allocation within a systematic framework.

The objective is not simply to be diversified, but to allocate more intelligently across changing market conditions: participate when opportunities are favorable, reduce aggressive exposure when risk expands and maintain a disciplined process without leverage, short positions or constant trading.

For long-term investors, this offers a more active and risk-aware alternative to a static portfolio.

Rules, constraints and risk controls.

The engine evaluates price behavior, relative strength, volatility and macro-sensitive conditions. When conditions justify it, the model adjusts the portfolio toward consolidated target weights. When risk rises, it can return toward a base allocation or reduce excessive exposure to the most aggressive sleeve.

- Base allocation framework with scheduled normalization.

- Event-driven tactical adjustments when predefined conditions are met.

- Volatility and trend controls designed to reduce whipsaw and late-risk exposure.

- Macro sleeve intended to improve robustness outside a single equity-growth environment.

- Cost-aware simulation and operationally simple target-weight instructions.

From signal generation to disciplined execution.

Model check

The engine evaluates current market data and portfolio state through a multi-layer rule set developed and reviewed over time.

Alert event

If an action is required, a private Telegram alert identifies the event and consolidated target allocation.

Execution instructions

The subscriber receives clear instructions to translate the target allocation into broker-level orders.

Audit trail

Signals, dates, weights and execution assumptions are internally tracked for review and coherence checks.

Clear alerts, disciplined execution.

Alerts are designed to be simple, actionable and easy to follow: strategy name, event type, signal date, execution instruction and consolidated target allocation.

Tactical Strategy does not offer copy trading. Its multi-instrument, target-allocation nature is not well suited to standard copy-trading platform formats, so it is offered as a manual alert service for disciplined investors.

Execution is intended only for brokers where all required instruments are available and where dividend/distribution reinvestment can be enabled when available.

Performance, risk and robustness are evaluated together.

Results are simulated net results using proxy PPA historical data and the internal engine. This version uses the PPA-only proxy structure: the portion that would otherwise be assigned to the additional defense sleeve is incorporated into PPA, allowing a longer public historical evidence window.

Designed to compete through smoother compounding.

The public simulation compares the strategy against an U.S. Equity Proxy Benchmark for context. The goal is not to mimic the benchmark, but to improve the balance between return, drawdown and recovery behavior.

| Metric | Strategy | U.S. equity proxy |

|---|---|---|

| CAGR | 22.47% | 15.26% |

| Max drawdown | -11.36% | -31.59% |

| Volatility | 12.72% | 16.55% |

| CAGR / Vol | 1.77 | 0.92 |

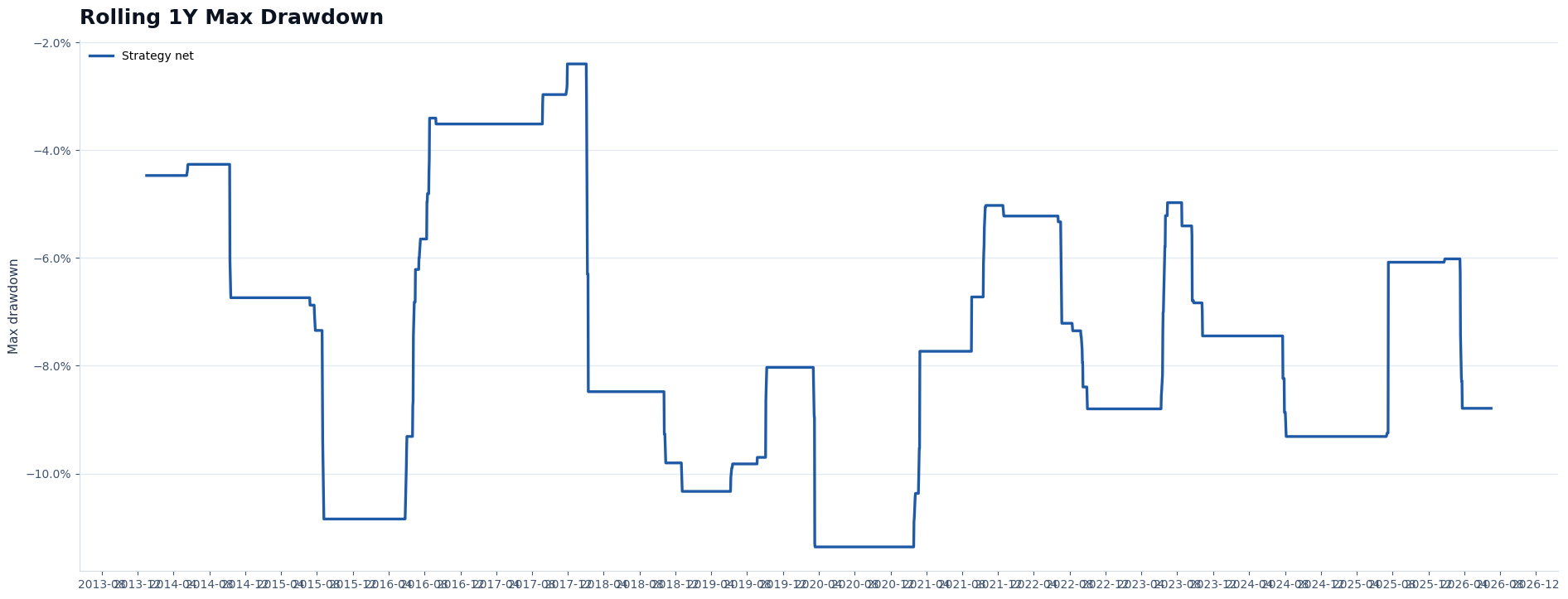

Risk is monitored as a first-class metric.

The strategy is evaluated through maximum drawdown, recovery time, ulcer index, tail behavior, rolling performance and cost sensitivity. The intention is to avoid a portfolio that looks attractive only because of a narrow historical window.

Strong uninterrupted bull markets may cause the strategy to underperform a fully exposed benchmark. That trade-off is part of the design: the strategy prioritizes smoother participation over maximum beta.

Not just one good backtest.

Rolling windows are used to detect performance concentration, regime dependence and degradation. Monte Carlo block bootstrap is used as an additional robustness check. In the public run, median MC CAGR is 23.11%, with a 5th percentile of 16.74% and a 95th percentile of 29.30%.

The model can be internally audited and reviewed periodically. Parameters are not changed automatically just because time passed; candidate changes must pass robustness and operational-coherence gates.

Manual, broker-aware and operationally disciplined.

Manual alert service

Tactical Strategy is not offered as copy trading because its multi-instrument, target-allocation nature is not well suited to standard copy-trading platform formats. Subscribers receive manual alerts and clear implementation instructions.

Eligible brokers only

The strategy should be used only where all required instruments can be traded correctly and position sizes can be implemented with adequate precision.

Dividend/distribution handling

Automatic reinvestment of dividends or distributions is recommended where available, so implementation remains aligned with the fully funded total-return intent.

Internal review and optimization discipline.

Ongoing monitoring

Rolling returns, drawdowns, volatility, signal frequency and behavior around stress periods are monitored to detect degradation.

Periodic research review

The strategy may be internally reviewed and optimized from time to time through a formal process that prioritizes robustness, practical implementation and long-term consistency.

Change gates

Candidate updates must improve risk-adjusted behavior, avoid overfitting and remain coherent under costs, delays and alternative market regimes.

For investors seeking a systematic allocation process.

Azimuth Tactical Strategy is designed for investors who prefer rule-based portfolio management, intelligent allocation rules, ongoing evaluation and disciplined signal execution over ad-hoc discretionary decisions.

Past performance, simulated performance and backtests do not guarantee future results. Investors can lose money.